March 2023

Solving the Rural Water Payment Puzzle: How to Improve Water Management in Uganda

Poor transparency and repeated misuse of community water point funds erode trust in the volunteers in charge of payment collection.

Access to safe and sustainable drinking water is a critical issue in many rural communities around the world, and the Kabarole district in Uganda is no exception. In this area, limited and inconsistent payments at rural water points have hindered efforts to achieve universal coverage of safe and sustainable drinking water supplies. The main problem stems from poor transparency and repeated misuse of community water point funds, which erodes trust in and authority of voluntary water user committees tasked with collecting user fees. This, in turn, lowers the willingness to pay, leaving most rural communities with insufficient revenue to fund repairs and at risk of extended periods without water [1] [2].

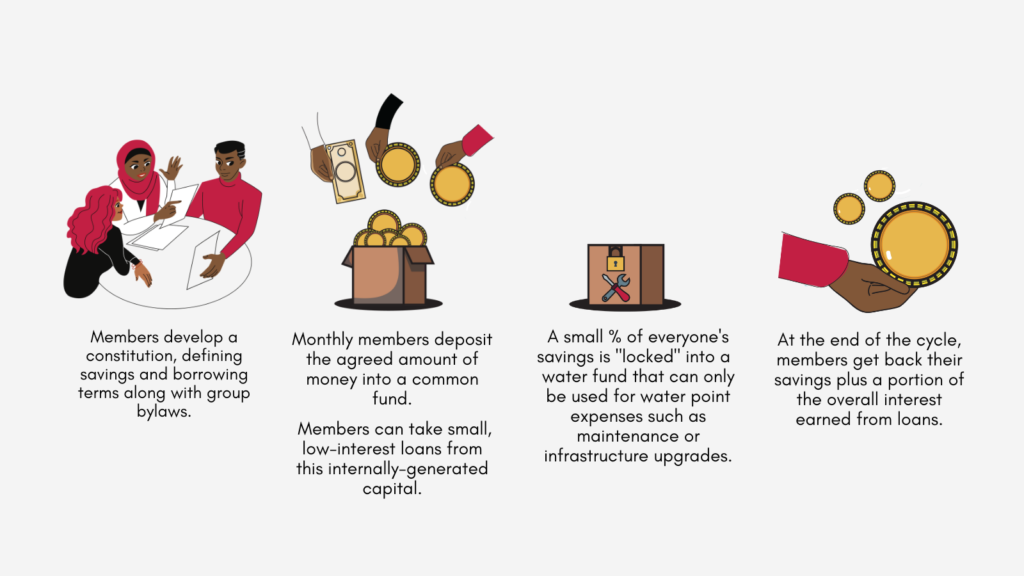

Village Savings and Loans Associations have robust accountability mechanisms.

To address this issue, Aquaya introduced and evaluated village savings and loans associations (VSLAs) as a solution. This was to promote consistent water user payments and influence additional safe water management practices. VSLAs are community-based groups that allow members to pool capital and access low-interest loans. These groups incentivize participation by providing multiple economic and psychosocial benefits to members. Further,well-managed VSLAs have robust accountability mechanisms that reinforce trust among members [3].

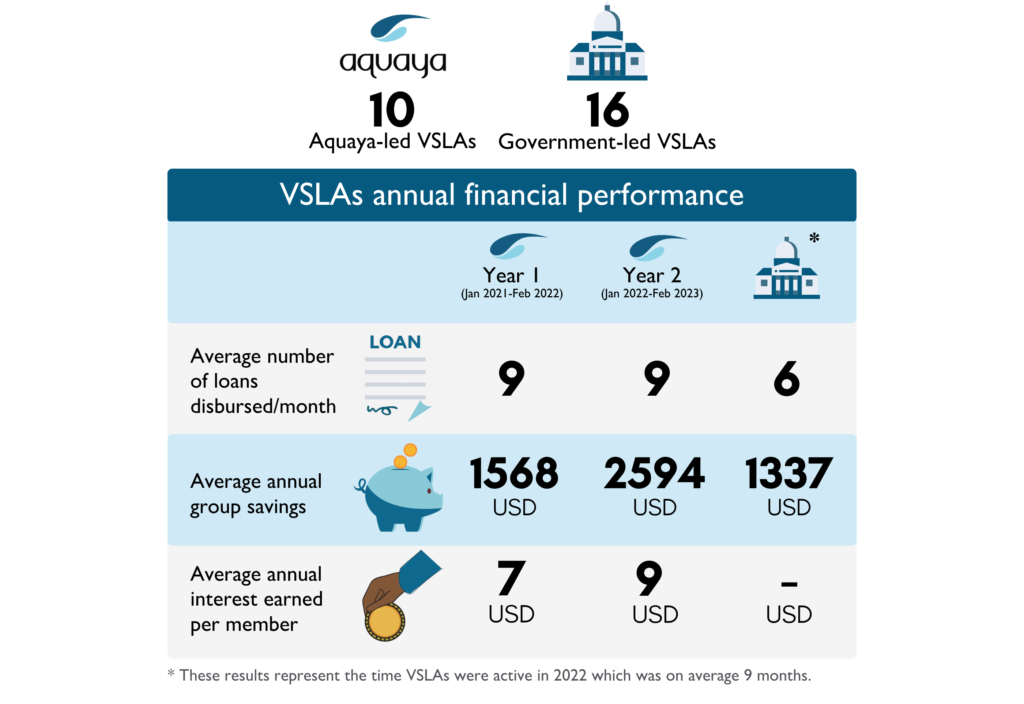

All VSLAs actively provided financial services to their members.

From January 2021 to February 2023, Aquaya collected data from Aquaya–led and government-led VSLAs in Kabarole district, Uganda. These data helped us understand the effectiveness of VSLAs in eliciting water user payments. The data also enabled us to comprehend the dynamics that influenced the performance.

All VSLAs actively provided financial services to their members. They disbursed an average of 8 loans per month, and this did not vary much between Aquaya–led groups and government–led groups or between the first year and second years. In the first year, on average, Aquaya–led VSLAs saved 1,568 USD and generated 361 USD in interest from loans, earning the average member a 7 USD profit. This increased in the second year to an average savings of 2,594 USD and 401 USD of interest, with the average member making a 9 USD profit. In their first 6-11 months, the 16 government–led VSLAs saved an average of 1,337 USD.

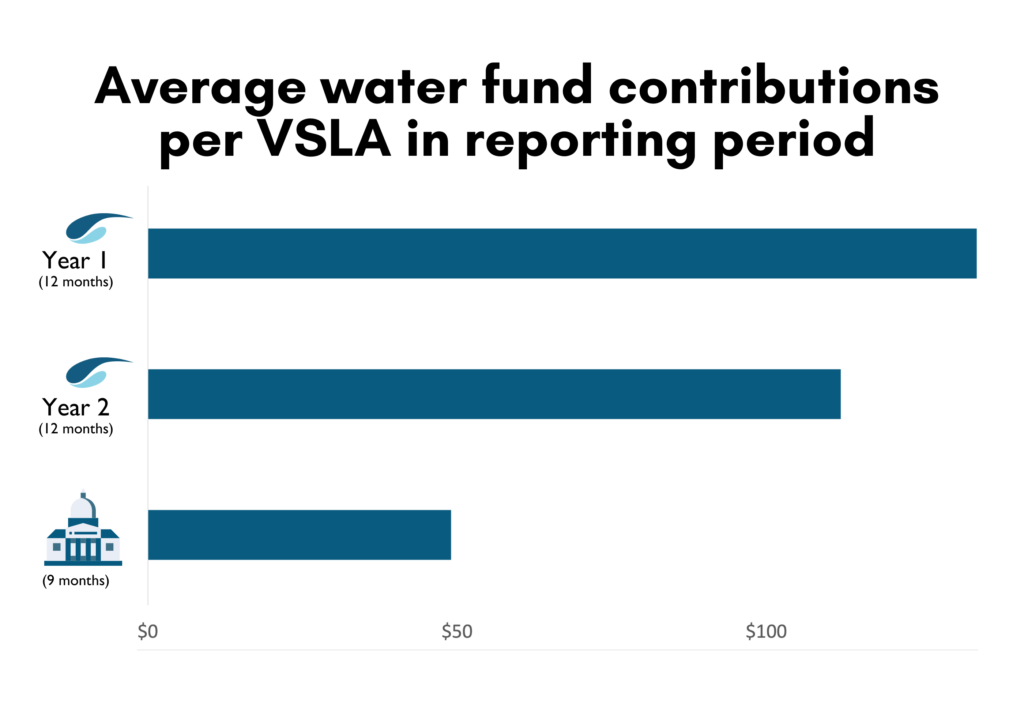

VSLA–based “water funds” can elicit regular community payments for water point management.

For the ten Aquaya–led VSLAs, generally, the amount of water fund contributions remained similar from the first to second annual cycles, with an average of 123 USD collected. This amount is usually sufficient to cover annual operations and minor maintenance provided by local mechanics [4]. The government-led VSLAs, on average, collected approximately half as much in water payments as the ten Aquaya–led VSLAs.

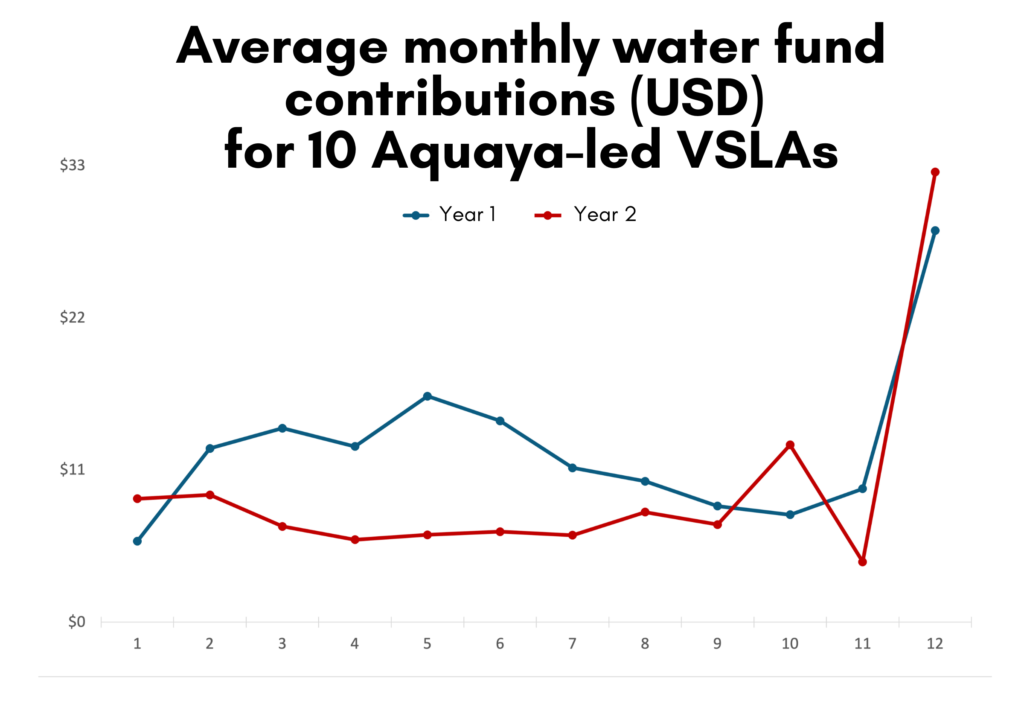

Water fund contributions fluctuated over time, but in most months, the majority, and often all, of VSLAs collected some payments. Further, the majority of all VSLAs used water funds for source protection measures, general cleaning around the water point, and/or minor maintenance.

Relatively stable water fund contributions over two years show promise for using VSLAs to collect water user fees. An overall increase in personal savings from the first to second year indicates members’ satisfaction with the VSLAs. Further, in the second year, Aquaya–led VSLAs operated autonomously and expressed fewer complaints. All ten initially Aquaya–led VSLAs rolled into a third annual cycle.

For the government-led VSLAs, less external support from Aquaya in the first year likely contributed to lower performance, though these VSLAs led to improvements over the status–quo of no water payments. Despite the lower performance, implementing the VSLA–based “water fund” approach via government staff may allow for cost-sharing between external NGOs and local government while bolstering interest and capacity among local actors to provide ongoing support.

Village Savings and Loans Associations can improve water management in Uganda.

Uganda’s National Framework for Operation and Maintenance of Rural Water Infrastructure [5] views water user payments as the primary funding mechanism for operation and maintenance; however, this framework will remain impractical without strategies to increase willingness to pay among rural water users. Following the first two annual cycles of the ten pilot VSLAs and the 16–VSLA district expansion, Aquaya, and Kabarole District Local Government remain encouraged about the potential of VSLA–based “water funds” to support water point management. Therefore, we are considering opportunities to evaluate VSLAs on a larger scale to understand better the factors driving the performance and potential durability of VSLAs to support water point management.

The Aquaya Institute is grateful for financial support from the Conrad N. Hilton Foundation.